Last month (May 2018) Login VSI and Frame presented the results of their State of the VDI and SBC union world-wide survey – the 2018 edition. Mark Plettenberg (Product Manager at Login VSI) and Ruben Spruijt (CTO at Frame) have put together a 66-page document holding all kinds of interesting VDI and SBC related statistics. The survey was completed by 755 people worldwide – go here to download your own copy. I went through the report and picked out a couple of subjects which are currently of most interest, or to me anyway.

SBC is still ‘a (big) thing’

According to the survey, there are currently more SBC based environments when compared to 2017. However, there is a slight decrease in newly designed, to be rolled out SBC deployments, a decline of 0,8% when compared to a year earlier – next to nothing if you ask me.

The use of VDI has also increased by 5%, it went up from 77% in 2017 to 82% in 2018. Both SBC and VDI environments are actively running in production for 2 to 4 years, or 5 years and above. For VDI, newly deployed environments declined from 3% to 1.18% in 2018. The rise of DaaS and Application Remoting will have something to do with this, though, I have to say that I find these numbers to be on the low side. Landscapes and strategies are changing, surely but slowly.

CTX vs. VMW

While Citrix is still the clear leader when it comes to SBC platform (s) / broker (s) used, they do show a slight decline – 6%. The competition, however, VMware, in this case, doubled their numbers up to over 16% market share – based on survey results. Not surprising if you look at what VMware has been doing throughout the last year and a half, or so. Their portfolio is near to on par with what Citrix has to offer (still some room for discussion here) and the team they have assembled on the End User Computing side is impressive, to say the least.

Almost 27% is running their SBC/VDI workloads on Windows Server 2008 (R2) – bare metal or virtualized. Note that with XenApp / XenDesktop 7.18 (just released) this OS is no longer supported – 2012 R2 and 2016 only.

The percentage of participants who consider changing their on-premises SBC/VDI brokers is stable, around 55%. Some of the other statistics tell us that these tend to lean more towards VMware, while others (12,57% in 2018) are considering cloud-based SBC/VDI options instead. Here it also needs to be noted that over 47% are still in doubt or investigating if an SBC/VDI cloud solution (DaaS/IaaS/Application Remoting) is a valid option/replacement, while almost 20% have already stated not be interested in such a solution at all.

Cloud alternatives

When thinking about a cloud SBC/VDI alternative, most are considering VMware, Citrix, and Microsoft. The interest in Amazon Workspaces (and AppStream) has declined, from 7.17% in 2017 to just short of 4% in 2018 – a shame, I would advise you to have a closer look at AWS Workspaces, it’s worth it. Interesting enough, this is where Citrix clearly beats VMware. Over 18% of the participants have indicated that they are interested in Citrix Cloud, while only 3.23% are considering VMware cloud offerings.

Now that more and more CSP’s can and probably will leverage the Microsoft CSP licensing model around Windows 10, making it possible (or legal) to host true Windows 10 desktops (license wise) from public and private clouds, I’m sure this will have a positive impact on future consumption of DaaS services globally.

With regards to Remote applications and Desktop as a Service provided by a service provider, Frame, on both AWS and Azure is considered by 8.7%, which is a solid increase coming from6.93% compared to 2017. Workspot also went up from 5.61% in 2017 to 8.71% in 2018.

The biggest competitor for public cloud DaaS/remote application as a service isn’t Citrix, Frame, Amazon, VMware, or Microsoft – it’s the on-premises VDI/SBC solutions combined with trends to use more web/SaaS, mobile, and PCs.

Community power

The survey states that historically the Citrix community is, or has been stronger and more active compared to the VMware EUC community – I doubt that. I’m not as active within VMware communities as I have been for Citrix, but there’s plenty going on for sure. The number (and size) of VMware community events nowadays is impressive, as is the number of active bloggers, book authors and such. So, even if the Citrix community was stronger, I’m not so sure that’s the case today.

User Environment Management

Here, Citrix, VMware, and Microsoft lead the pack. They make-up 76.2% In total. Which makes me wonder, is that because they have the best UEM solutions? I don’t think so. Often, UEM is already part of the package (license wise) so why buy anything else. And I do not mean to be negative here, because they are good solutions. However, I do feel that there are better, or perhaps I should say, more complete solutions out there. Especially now that Windows 10 migrations are a #1 priority when it comes to key EUC initiatives for 2018/2019 – one of the survey question as well. Of course, the overtake by Ivanti hasn’t helped either, it might turn out fine in the long run but for now tons of existing customers are in doubt if they should continue/renew to use RES since its future is ‘cloudy’ to say the least.

Traditional (not legacy) applications

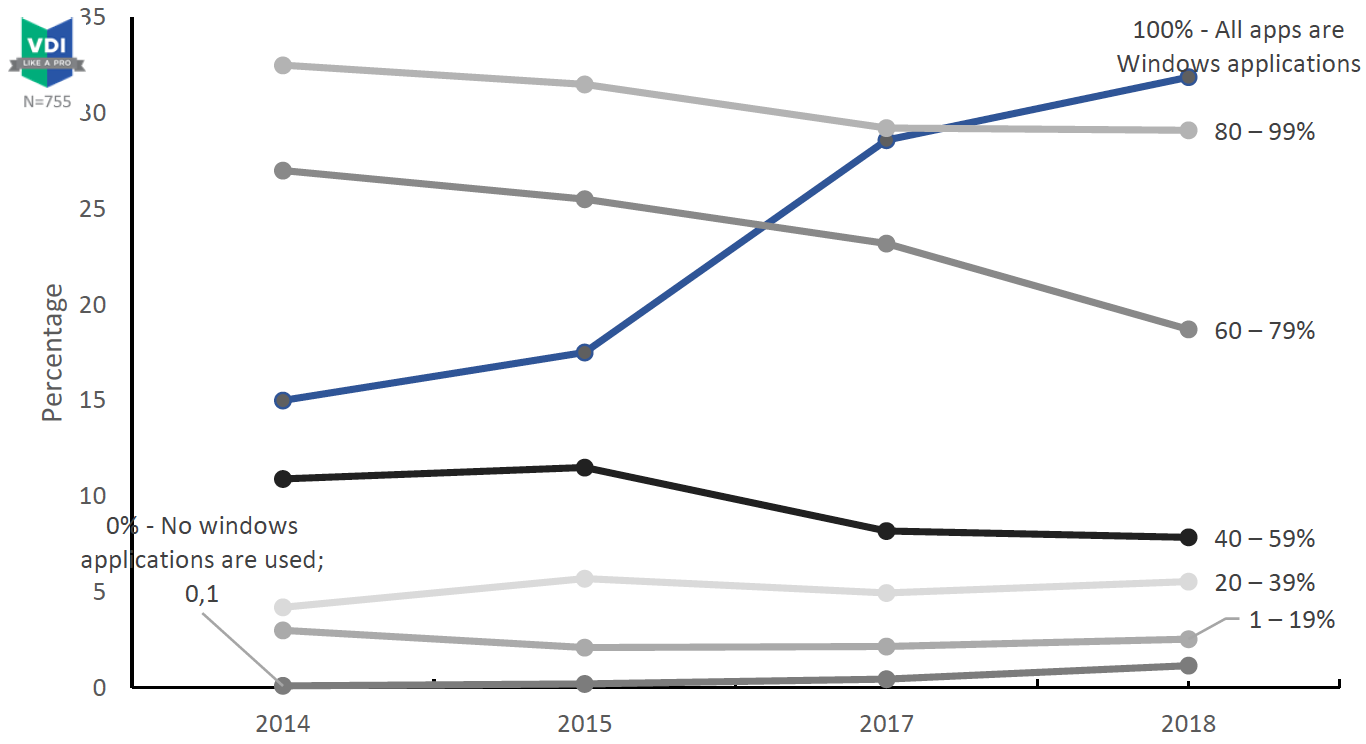

Just joking, of course. I get why people call Windows applications legacy, I just don’t fully agree. Anyway, having a look at the survey not that much has changed throughout the past few years. Traditional (Windows) applications still rule the universe – born in the 80’s? You see what I did there, right? If you do some quick, though not extremely augurate math, you’ll notice that on average 75% of all applications are (still) Windows applications. In fact, if you have a look at the graphic below, you’ll see that the use of Windows applications (in the case of 100%) has again gone up. New types of applications e.g. SaaS, Mobile, Universal, etc. will slowly bring this number down in the years to come, I’m sure.

Just joking, of course. I get why people call Windows applications legacy, I just don’t fully agree. Anyway, having a look at the survey not that much has changed throughout the past few years. Traditional (Windows) applications still rule the universe – born in the 80’s? You see what I did there, right? If you do some quick, though not extremely augurate math, you’ll notice that on average 75% of all applications are (still) Windows applications. In fact, if you have a look at the graphic below, you’ll see that the use of Windows applications (in the case of 100%) has again gone up. New types of applications e.g. SaaS, Mobile, Universal, etc. will slowly bring this number down in the years to come, I’m sure.

App virtualization vs. layering

Roughly 30 to 40% of the above highlighted Windows applications are, or cannot be virtualized. Who doesn’t want to create abstraction layers making it easier to update and manage your golden images, right?! Well, with application layering you can! Assuming there isn’t a direct SaaS alternative available, which won’t be the case for most.

66.59% have indicated not to be using any form of application layering (up over 7% from 2017). I see a huge opportunity here, not just for app layering vendors, but for the admins/customer base involved as well. I know there’s a saying, what we don’t know – we fear, but trust me, it’s not scary, at all, or difficult to get your head around. Citrix currently leads the pack on this one with almost 14%, I wonder how many are ‘ex’ Unidesk customers though. Yeah, I know, I worked for Liquidware before, but even prior to that FlexApp came out on top, worth a look and try.

Office 365 and stateless

Over 30% indicate to be using Microsoft Office 2016 as part of an Office 365 offering. No real surprises here, expect these numbers to rise significantly in the years to come. Also noticeable is the percentage of both Office 2010 and 2013, respectively 15.18% and 25.3%.

If we combine this with another statistic, the percentage of stateless/pooled VDI desktops that are being used globally (and SBC of course), the challenges we have around locally cached .OST files and the roaming of the (Outlook) search index will become even more prominent. Luckily, there are multiple solutions to choose from, which help us to overcomes issues like these. Even Citrix has been working hard to incorporate this into their UPM/WEM products, as have Microsoft as part of the upcoming Server 2019 Operating System, have a look here.

Concluding

- It is clear that the ‘traditional’ way of implementing SBC and VDI’s is still very popular.

- On-premises deployments are still huge – bigger than in 2017 even. The decline in new deployments is almost neglectable.

- Both SBC and VDI deployments are often running for up to 4 years, or longer.

- This might lead to a ‘big bang’ where older, and larger environments will be cloudified on large scale somewhere in the next few years.

- Citrix leads the pack but is losing terrain (on-premises) on VMware (up almost a 100%).

- VMware has been very active in the EUC field (in a positive way), their dream-team and communities included.

- Cloud solutions are gaining ground, slowly still, but surely. I think the numbers go well with what I see and hear as well.

- When it comes to SBC/VDI/DaaS from the cloud the biggest chunk of respondents is choosing Citrix over VMware.

- Amazon Workspaces are not getting the love they deserve, though, of course, that’s a personal opinion.

- Application Virtualisation is being implemented on a massive scale, more even when compared to 2017 – plenty of gaps still to be filled though.

- There’s a huge opportunity regarding Application Layering, the market is still wide open. No, I don’t see SaaS solutions taking over this market anytime soon.

- Traditional Windows applications still rule the universe – see the previous bullet, same SaaS rules apply.

- Office 365 is growing fast (and pooled/stateless workspaces are still used by most) thus the index roaming and local .OST caching challenges will become more apparent as well.

- The big three lead the pack when it comes to UEM solutions. This space is rapidly changing – I’m already looking forward to the numbers of next year.

All in all, a very nice and detailed report! Of course, there’s a ton of info I haven’t covered, so make sure to get your own copy and see what you make of it – this is simply a way (mine) of interpreting the data. And in case you might be wondering, I spoke to Ruben and Mark personally before going into any details.